UPPER TRIBUNAL (LANDS CHAMBER)

UT Neutral citation number: [2023] UKUT 93 (LC)

UTLC Case Numbers: LC-2022-507

Royal Courts of Justice,

Strand, London WC2A 2LL

TRIBUNALS, COURTS AND ENFORCEMENT ACT 2007

AN APPEAL AGAINST A DECISION OF THE VALUATION TRIBUNAL FOR ENGLAND

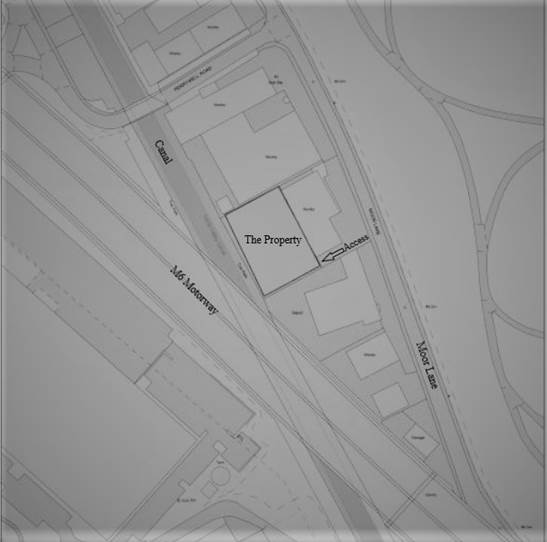

RATING - valuation - alteration of 2017 rating list - self storage site - rental evidence - evidence of other assessments - end allowance - appeal allowed - assessment determined at rateable value £17,100

BETWEEN:

DAL VIRK

(VALUATION OFFICER)

Appellant

-and-

MOOR LANE SELF-STORAGE LIMITED

Respondent

Re: Moor Lane Self Storage ADJ,

1 Moor Lane,

Birmingham,

B6 7AE

Mr Mark Higgin FRICS FIRRV

14 March 2023

Decision Date: 18 April 2023

Mr Brad Davies of the Valuation Office Agency for the appellant

Mr Paul Rabbette of Rabbette Chartered Surveyors for the respondent

Introduction

1. This is an appeal by the Valuation Office (‘the VO’) against a decision of the Valuation Tribunal for England (“the VTE”) dated 14 September 2022, in which it determined an appeal against a decision notice issued by the Valuation Officer (“the VO”) at a rateable value of £12,250 for Moor Lane Self Storage ADJ, 1 Moor Lane, Birmingham, B6 7AE (“the Property”). The effective date of the decision was 8 April 2017 this being the date on which the Property was first entered in the rating list. It is described in the rating list as “Land Used for Storage and Premises”.

2. In this appeal the appellant sought to increase the VTE’s determination to a rateable value of £17,500 whilst the respondent sought to retain the decision.

3. The case was conducted under the simplified procedure. The appellant was represented at the hearing by Mr Brad Davies who called Mr Haroon Bhatti BSc(Hons) MRICS, as an expert witness. Mr Bhatti is a Valuation Lead Caseworker at the Birmingham office of the VO. The respondent was represented by Mr Paul Rabbette MRICS, Managing Director of Rabbette Chartered Surveyors based at Pershore in Worcestershire. He acted as both advocate and expert witness. I am grateful to them all for their assistance.

4. I inspected the Property on 10 March 2022 accompanied by Mr Bhatti and Mr Rabbette. On the same day I inspected comparable properties in the greater Birmingham area, and I will examine these in detail as part of the decision.

The facts

5. The Property comprises a yard which appears approximately rectangular in shape but is in fact a trapezoid having four sides of unequal length none of which are parallel to one another. The average dimensions were said by Mr Bhatti to be 45.35 metres and 32.15 metres. The longest side is arranged on a north west/south east axis. The yard has a concrete surface and the land on which it is built is sloping with a difference in height of about a metre. The overall gradient between the front and rear boundaries could therefore be said to be roughly 1 in 32.

6. In early 2017 the owner of the site, who also owns the neighbouring factory behind which the Property is situated, decided to commence trading as a self-storage business. This involved placing shipping containers on the Property for the use of businesses, organisations and private individuals. The containers need a level surface on which to sit and the site is therefore arranged in two tiers with a retaining wall between them. Concrete slopes at either end allow vehicular access. According to measurements taken on site by Mr Rabbette, the upper tier measures 44.3 metres in length and is 15.6 metres wide. It contains two rows of standard 20ft containers, one of 18 and another of 11. Two smaller 10ft containers flank the ends of the smaller row. The lower tier is slightly longer at 44.9 metres but narrower, having a width of 14.2 metres. It similarly contains two rows of containers, but the confines of the site mean that the layout is different. The smaller row contains 8 small 10ft, and 2 standard 20ft containers whilst the other row has 14 standard 20ft and 1 small 10ft containers. One of the standard containers has been adapted as a site office. The parties have agreed that there are in total the equivalent of 49 standard 20ft containers.

7. The Property is located on the western side of Moor Lane in an area which is largely industrial in nature. It lies some 3.25 miles north of Birmingham city centre and just to the north of an elevated section of the M6 motorway. Access to the motorway is at ‘Spaghetti Junction’ about 1.25 miles to the south east of the Property. The Tame Valley Canal effectively forms the south western boundary of the site. The plan below shows the relationship of the Property to its surroundings:

8. The respondent owns the freehold of the Property.

Statutory background

9. Rateable value is defined in Paragraph 2(1) to Schedule 6 of the Local Government Finance Act 1988, as amended by The Rating (Valuation) Act 1999 as: "... an amount equal to the rent at which it is estimated the hereditament might reasonably be expected to let from year to year on these three assumptions:

a) the first assumption is that the tenancy begins on the day by reference to which the determination is to be made;

b) the second assumption is that immediately before the tenancy begins the hereditament is in a state of reasonable repair, but excluding from this assumption any repairs which a reasonable landlord would consider uneconomic;

c) the third assumption is that the tenant undertakes to pay all the usual tenant’s rates and taxes and bear the cost of the repairs and insurance and the other expenses (if any) necessary to maintain the hereditament in a state fit to command the rent mentioned above.”

10. Statute requires that the appeal Property be valued reflecting certain matters as they existed on the material day, which for the 2017 Non-Domestic Rating List is 1 April 2017, and by reference to values pertaining at the Antecedent Valuation Date (AVD) which is 1 April 2015. The matters which must be taken at the material day are set out in paragraph 2(7) of Schedule 6 Local Government Finance Act 1988. The matters relevant to the appeal are:

(a) matters affecting the physical state or physical enjoyment of the hereditament;

(b) the mode or category of occupation of the hereditament;

(c) ....

(d) Matters affecting the physical state of the locality in which the hereditament is situated or which, though not affecting the physical state of the locality, are nonetheless physically manifest there;

(e) the use or occupation of other premises situated in the locality of the hereditament.

Valuation of self-storage premises

11. Before I examine the detail of the experts’ approaches to this particular Property it is worth noting that there does not appear to be a consensus about valuation methodology between the VO and the surveyors representing the operators of container self-storage sites. The containers themselves are readily available for purchase, most having arrived here as ‘single use’ or ‘one trip’ bringing goods from the Far East. Owing to global differences in manufacturing costs it makes better economic sense to dispose of the containers at their destination rather than re-use them. In this case I was provided with invoices showing that a ‘once shipped’ container cost £1,625 net of VAT in March 2017.

12. The Property was originally valued for the purposes of the 2017 rating list by applying a rate of £10 per m2 to a site area of 1,500m2 and then adding 48 containers at £150 each. At the ‘challenge’ stage the site area was refined to 1,458m2 but the addition for the containers remained unchanged.

13. The VTE decision was based on an area of 554.95m2, being the area of the site not covered by the containers. This was valued at £10 per m2 and the containers were again valued at £150 each. The VTE also applied a 5% end allowance for difficulties associated with the sloping site.

14. In this appeal the VO sought to revert to the site area and value determined at the ‘challenge’ stage but with an additional sum for the containers based on a decapitalised cost for each container of either £71.07 or £72.52. I will investigate these figures in detail later in the decision. The VO also sought an end allowance of 2.5% for the sloping site. I note that the container values do not accord with the VO Cost Guide which cites a figure of £65.91 per container or with the rate applied at other self-storage sites in Birmingham where £150 per container has been used.

The issues between the parties

15. There were four issues between the parties:

i. Should the whole site area be valued or just the area not situated under the containers? In other words, is the value of the land on which the containers sit reflected within the value of the container?

ii. If the whole site area is to be valued, what is the correct area?

iii. What is the correct value for the containers?

iv. Should there be an allowance for the sloping nature of the site and if so what would be an appropriate figure?

It should be noted that the parties have agreed that the site should be valued at £10 per m2 which is, as it were, a ‘ground rent’ which does not include any sum to reflect the presence of the containers.

Issue 1: Should the whole site area be valued or just the area not situated under the containers?

16. This was the fundamental dispute between the parties and the largest in terms of value. Mr Bhatti explained that his view was that all the land at the Property should be treated equally and that the value of the land on which the containers were placed was not extinguished simply by the presence of the container. He said that there was no rental evidence for container based self-storage in the Birmingham area but there were leasehold sites used for other purposes which had containers on them. He provided a list of seven sites in the greater Birmingham area with rents effective from a variety of dates ranging from 1 April 2012 to 1 Jan 2016. The uses the sites were put to were quite disparate and included car breakers yards, hand car washes, storage compounds and a retail outlet for timber sheds and fencing. Mr Bhatti had gleaned the information about each one from internal VO records and Rent Return Forms completed by the occupiers. He had undertaken a ‘drive-by’ inspection of each one but had not actually visited the sites. He had not included any detail about these transactions in his report other than the rent passing, an analysis and the effective dates. Only one site, at Kingsbury Road, Minworth, Sutton Coldfield was remotely comparable in size to the property. It occupied a much more prominent site on a major road within a few minutes’ drive of a junction of the M42. It was let at £16,800 per annum on lease that commenced on 1 April 2012. Notwithstanding that the value per metre squared for the Property was agreed, it would have been helpful to have more information about these sites, especially to discern whether anything useful could be deduced about the value of the containers.

17. Mr Rabbette had been much more diligent in his approach, visiting each of Mr Bhatti’s comparables as well as his own, taking photographs and providing the detail of the assessments together with a commentary. From his report I was able to determine that all but one of Mr Bhatti’s comparables were assessed at figures below the Small Business Rate Relief threshold for the payment of rates which made it unlikely that the assessments had been the subject of any investigations. Some of the rents related just to the sites, others to buildings as well. None of these sites were in the same mode or category of occupation as the Property but Mr Rabbette’s efforts were not entirely in vain as the detail of the assessments showed two approaches to the valuation of the containers. These were to value them at a spot figure of £20 each or at £20 per m2 in addition to the value of the land on which they had been placed.

18. Mr Rabbette’s report also identified three container based self-storage sites in Birmingham. Details of these operations had been provided by Mr Bhatti’s predecessor at the Valuation Tribunal hearing. I will deal with these in turn, but it was surprising, to put it mildly, to find that Mr Bhatti had not mentioned them at all in his evidence. He readily admitted in cross examination that he knew about them but had not thought it necessary to provide any details and had not inspected them either. Despite remarking in his report that he was appearing as an expert in accordance with the latest RICS Practice Statement, he seemed to have little awareness of his duty to the Tribunal to consider all the evidence and not simply select the information which supported his conclusions.

19. Returning to the sites in question, the first of these was:

K B Storage, Curzon Street, Birmingham, B4 7XE

20. This site was originally known as City Self Storage but has now been cleared to make way for the approach to Curzon Street HS2 station. It occupied a central position close to the A454 and city centre. Mr Rabbette had obtained a copy of the VO’s survey sheet from 2009 and it was obvious that they had accepted the occupier’s calculation of the site area of 1.1 acres rather than measuring it themselves. At that point in time there were 32 containers on the site but no addition for them in the assessment.

21. Mr Rabbette, after inspecting satellite images of the site, thought that there were 244 containers at the advent of the 2017 list. The details were as follows:

16 x 12.2 metre (40 foot) containers

165 x 6.1 metre (20 foot) containers

46 x 5.48 metre (18 foot) containers

17 x 3.05 metre (10 foot) containers

He had used Google Earth Pro to estimate the size of the site as 1.64 acres or 6,636.85 m2. He calculated that the containers were occupying 3,898.59m2, leaving 2,738.26 m2 for circulation and access. He noted that the VO had taken a site area of 4,432.6 m2 which would mean that if his calculation of the container area was correct there would only be 534 m2 left for circulation. He thought this would not be enough land to access each container. In terms of the assessment in the list the VO had used a rate of £6.80 per m2 for the site and £150 per container with no differentiation for size.

22. Mr Rabbette concluded that this evidence was inconclusive as the VO appeared to have used an incorrect site area. I agree, and I also take the view that little weight should be placed on this comparable as there are significant discrepancies between the site area in the assessment and that calculated by Mr Rabbette. Unfortunately, owing to the HS2 works it is no longer possible to verify either on the ground.

Fort Parkway, Birmingham, B24 9AW

23. Mr Rabbette confirmed that this site had not been the subject of a challenge on the 2017 rating list. From my own inspection I noted that it is located under an elevated section of both the M6 motorway and the A47 Fort Parkway. It is situated about 3 miles north east of Birmingham city centre and 2.5 miles south east of the Property. Access to the site is only from the west bound side of the Fort Parkway dual carriageway.

24. The current assessment which was effective from 11 October 2019 comprises 8,778 m2 of unsurfaced, fenced land valued at £5.42 per m2, 294 containers at £150 each and an office of 60.5 m2 assessed at £50.00 per m2. It is worth noting that at the time of my visit the yard had a concrete surface and this was also clearly shown in Mr Rabbette’s photographs. Mr Rabbette had again turned to Google Earth Pro to estimate the size of the site and he had arrived at an area of 12,597 m2 but acknowledged that this exercise was difficult as part of the site was concealed beneath the elevated roads. He had also spoken to the owner of the site who had confirmed that the site extended to just under four acres and the company’s website stated that it was 3.8 acres or 15,378.1 m2.

25. Mr Rabbette’s Google Earth Pro investigations revealed that there were at least 305 containers of various sizes on site. However, some were under the elevated roads and he was therefore unsure of the total number. Using the actual number of containers that he could see on screen he arrived at an area for the containers of 4,606.42 m2. Adopting either the owner’s site area or his own it appeared to Mr Rabbette that the VO had not valued the land under the containers.

Bluloc Self Storage, Thimble Mill Lane, Birmingham

26. This was the only site amongst the three container based self-storage premises that had been the subject of a completed challenge although the analysis supplied by Mr Rabbette related to the assessment effective from 1 June 2019 rather than the beginning of the list.

27. The site is located about two miles north of the city centre, close to the A5127 Lichfield Road. It is situated some two miles south of the Property and occupies a narrow site alongside the Birmingham & Fazeley Canal. The containers were arranged in two rows, one down either side of the site with an access area between them.

28. Mr Rabbette had identified this site as an important comparable and had asked the VO to disclose the detail of the assessment. In response they had sent him a copy of a request from the Billing Authority to the VO to reassess the site on account of an increase in site area and additional containers. Mr Rabbette had spoken to the chartered surveyor who had agreed the assessment, Mr Leigh Franklin who had provided details of his discussions in an e-mail to Mr Rabbettte dated 31 October 2022, and a copy was appended to Mr Rabbette’s report.

29. In the e-mail Mr Franklin said that there had been various amendments to the assessment between May 2018 and June 2019 as Bluloc had added containers from time to time. The site area had been agreed at 2,117 m2 but only 1091 m2 had been assessed at £10.08 per m2 together with 68 containers. Mr Franklin went on to confirm that the containers had originally been valued at £20 per m2, this basis having being derived from sites where the containers were ancillary to other buildings. Latterly, they had been valued at £150 each. Mr Rabbette had used his usual method of consulting Google Earth Pro to arrive at a site area of 2,089 m2 and had noted 65 standard 20ft containers, 1 of 15ft and another of 10ft. He was unsure of the date of the satellite imagery that he had used. When I inspected the site it appeared that part of it was in use by a company known as Taroni Motor Spares with access being by means of the area between the containers. Mr Rabbette confirmed at the hearing that he had spoken to a Mr Taroni who explained to him that he was the eponymous motor spares trader and the owner of Bluloc. He was therefore running two businesses from the same site. The Billing Authority had asked the VO to reassess the site, but they had delayed doing so until the outcome of this hearing was known.

30. Mr Rabbette had calculated that the containers occupied an area of 1,053.98 m2 leaving 1,063.02 m2 without containers. His conclusion was that the VO had not explicitly valued the area of the yard that the containers occupied. In his report he said;

‘This seems to indicate that the agreed approach to this assessment was not to explicitly value the land under the containers’.

Discussion

31. The first matter to address is the footprint of a standard 20ft container. Mr Davies in his submission stated that VO research showed the dimensions to be (in metric terms) to be a length of 6.1 m and a width of 2.44 m. Mr Rabbette had used a width of 2.59 m in his calculations. As 2.44 m corresponds to precisely 8ft and shipping container external dimensions are predicated on imperial measurements I am inclined to believe that Mr Davies is correct. This means that a 20 ft long container occupies an area of 14.884 m2.

32. I do not attach much weight to Mr Bhatti’s rental evidence. Only three of the seven rents quoted could have been known to a hypothetical tenant at the antecedent valuation date although in this particular market it is unlikely that prospective occupiers undertake detailed research in to passing rents before bidding. Only the Minworth site was comparable in size to the Property. Despite being more prominent, having a block paved surface and being used for retail it had the lowest analysis of any of the sites at just £3.77 per m2. In assessing the site for the 2017 list the VO had seemingly disregarded the rent and adopted a rate of £10.00 per m2. I share their reluctance to attach weight to it.

33. This leaves the three self-storage sites. I have already expressed reservations about relying on the KB Storage site at Curzon Street. The detail provided by Mr Rabbette related to a historic assessment based on an area that had not been authenticated on the ground. No evidence was provided of any kind of verification of the 2010 list assessment. Mr Rabbette had used his ‘best estimate’ to calculate the area and thought the evidence was inconclusive. I agree with him.

34. I have similar reservations about Fort Parkway. The facts are that the site area extends to 15,378.1 m2 according to the occupier, but Mr Rabbette’s Google Earth Pro calculations resulted in a figure of 12,597 m2, a difference of more than 18%. The VO have assessed an area in use of 8,778 m2 and believe there to be (as at 11 October 2019) 294 containers of indeterminate sizes. Mr Rabbette had done his best with satellite photographs to estimate the number of containers but his areas for the difference sizes of containers appear erroneous. Adopting his numbers of containers with the correct dimensions results in an area occupied by the containers of 4,341.8 m2, or in other words, just under 50% of the site area adopted by the VO. Mr Rabbette did not provide the date of the satellite imagery he used and it might well have been different to the particular assessment he had attempted to analyse. Some of the containers were obscured in the image. I would have found it very helpful to have had the VO’s clarification about how they approached the valuation but since Mr Bhatti had chosen to ignore this property this insight was not available.

35. The result is that this comparable is of limited use. Mr Rabbette surmised that adding the container and yard area together produced an area of 13,384.42 m2 and that the VO had not valued the area under the containers. Other plausible explanations are that the VO got the site area wrong or decided to only assess part of it. The fact that they assessed the containers at a flat rate of £150 each regardless of size does not in my view, indicate that their methodology was derived from an area based approach. Mr Rabbette’s conclusion is therefore questionable.

36. I turn finally to Bluloc Self Storage. It is clear that this site extends to about 2,100 m2. Mr Rabbette’s calculations need to be adjusted to reflect the correct dimensions and I therefore adopt a figure of 993.5 m2 for the area under the containers. This represents about 47% of the whole site. Mr Franklin’s e-mail did not say that the area under the containers was not valued. It says that 1,091 m2 was valued and a fixed price for the containers was adopted. Working with the information at hand it is possible that the parties agreed an area of 1,091 m2 for the containers and treated the remainder of the site as access and reflected the value in the land. It is simply not known with any certainty how the parties approached the value of the land.

37. The parties are agreed that the Property should be valued at £10.00 per m2. Mr Rabbette agreed at the hearing with the proposition that if the site was cleared of containers its value would be the whole area taken at £10.00 per m2. Following his methodology of excluding the value of the land under the containers would mean that the site is worth substantially less with the containers in place than it is without. That seems to me to make very little sense. The hypothetical landlord would hardly spend £1,625 per container on setting up a self-storage hereditament if in so doing he diminished its value by a significant margin.

38. Mr Davies observed that if a container is worth £150 per annum in rent then using the gross area of a 20ft container it would command £10.08 per m2. Simply adopting the value of the container as both the value of the land and the container would translate into a value for the space in the container at the Property of £0.08 per m2 which was clearly nonsensical. Mr Rabbette said that deducting the annualised cost of the container of £65.91 (derived from the VO Cost Guide) from the £150 rental value showed the annual value of the land on which the container sat to be £84.09 or £5.65 per m2. The obvious flaw in this approach is that where the site value was less than £5.65 per m2, placing a container on it would result in a negative value for the land.

39. I am not convinced by Mr Rabbette’s argument. The Property is open storage land with items placed on it. In that regard the containers are no different to a portakabin or an item of plant and machinery placed on the land. A container is not a permanent structure and whilst it was agreed between the parties to be rateable whilst on site it is not attached to the site in the way that a conventional building would be. Notwithstanding what has happened at the three self-storage sites relied upon by Mr Rabbette, in my judgement the correct methodology for the valuation of the Property is to value the whole site with an addition for the containers.

40. In Storehouse (UK) Limited v Wojcik (VO) [1991] LT RA 39 the Tribunal (C R Mallett FRICS) considered the assessment of a containerised storage yard at Stansted Airport. The Member concluded that:

‘I have come to the conclusion that the 48 containers in this case are, as a matter of fact, chattels which are in the nature of structures in the exclusive occupation of the ratepayers enjoyed with the land forming the compound and together with that land forming a ratable hereditament.’

He went on to say:

‘What distinguishes this case is:

(1) The intention of the ratepayer to keep at least 48 of the containers on the land for the purposes of hiring storage space on that land, for a period that is more than transient.

(2) The fact that the use of the containers is essential to the ratepayer’s business.

(3) The fact that the use of the containers is essentially with the land forming the compound.’

It would be wholly incorrect in my view, to value a hereditament where the chattels are intrinsic to the operation of the business by completely discounting the value of the land on which they are located. The use of the containers is with the land which cannot be used for its more valuable secure storage purpose without the presence of the containers. Given the nature of self storage operations it is very unlikely that there will be any open market rental evidence for sites with the containers in place but whatever method of value is deployed to ascertain the enhancement it must be in addition to the value of the land itself and not in place of it. Neither expert considered whether the hereditament, as a self storage site, should attract a value in excess of the aggregate value of the components.

41. In his report Mr Rabbette referred me to the decision of the Tribunal in Futures London Ltd v Stratford [2005] EW Lands RA/47/2005 (P H Clarke FRICS) to make the point that for small hereditaments where there is no liability a tone cannot be inferred from a lack of challenge. The Member said at paragraph 25:

‘When an assessment is challenged before a tribunal the correct time for deciding whether the tone of the list has been established is immediately before the hearing. The weight to be given to comparable assessments as evidence of value will depend on the circumstances in each case. These may indicate that little or no weight should be given to comparable assessments, eg where acceptance of value is more acceptance of rate liability or where a body of settlement evidence rests on a single agreed assessment.’

I understand Mr Rabbette’s point but it is relation to Bluloc that the Member’s remarks are pertinent. In this case there is not a body of settlement evidence resting on one agreed assessment, I have simply been provided with one agreed assessment and an interim one at that. I decline to place much weight on it.

Issue 2: If the whole site area is to be valued, what is the correct area?

42. There was no agreement between the parties as to the overall size of the site. Mr Bhatti’s area was 1,458.0 m2 whilst Mr Rabbette’s amounted to 1,328.66 m2. Mr Bhatti had used the VO’s proprietary digital mapping software to calculate the area whereas Mr Rabbette had used a measuring wheel. The differences in dimensions were not sufficient to explain why the parties’ figures were so disparate. At the hearing Mr Rabbette handed up a copy of his site plan and measurements. From this plan it was possible to deduce that his area was the aggregate of the areas of the two tiers rather than being based on the whole area of the site. His total dimension for the width of the site at the southern end matched Mr Bhatti’s but the dimensions of the longer sides were smaller. Having recalculated Mr Rabbette’s areas using the overall dimensions I find his area to be 1,449.5 m2. Splitting the small difference between the two parties I determine the site area to be 1,453.75 m2.

Issue 3: What is the correct value for the containers?

43. From the assessment evidence before me there is no consistent approach to the valuation of storage containers in the Birmingham area. Containers have been valued for the 2017 rating list at flat rates of £20 or £150 per container regardless of size, or at £20 per m2. Mr Bhatti’s statement of case promulgated a figure of £65.91 per container, said to be derived from the VO Cost Guide. By the time he filed his expert report he had refined his approach further. He referred to a rate of £71.07 per container which included the Cost Guide pricing of £1,458 together with the cost of purchasing and siting the containers at the Property. The costs were derived from invoices supplied by the respondent and dating from March 2017, two years after the AVD. The total cost was decapitalised at 4.4%, being the statutory rate for use in contractors test valuations. He had not made any adjustment for inflation between the AVD and the date of purchase. He also put forward an alternative approach in which he used the actual 2017 costs adjusted by 5.4% to take account of the change in the Retail Prices Index between the AVD and March 2017. The result was again decapitalised at 4.4% resulting in a figure of £72.52 per container.

44. Mr Rabbette endorsed the approach of the VTE who had adopted a value of £150 per container.

Discussion

45. An approach which adopts the same value for a container regardless of its size or cost does not, it seems to me, have much to recommend it. However, in the absence of any rental evidence or information on which to base a receipts and expenditure valuation there is no option but to adopt a cost-based approach.

46. The VO cost guide refers to a figure of £1,498 per container and it is likely that the use of this figure is widespread across a variety of contexts. I am inclined to the view that where the actual costs are known then they should be the starting point. Invoices supplied by Mr Bhatti show that the containers cost £1,625 each with delivery at £97.25 each and he had applied an additional £20 per container for siting. There was no evidence for the latter increment, and I therefore disregard it. It is necessary to adjust the costs for inflation between the AVD and the date of delivery and Mr Bhatti had used 5.4% being the increase in the Retail Prices index between April 2015 and March 2017. Adopting Mr Bhatti’s approach I arrive at the sum of £1,634 per container as at the AVD. The only remaining adjustment is the selection of the appropriate rate at which to decapitalise the cost of the container.

47. In Bunyan (VO) v Acenden Limited [2023] UKUT 17(LC) the Tribunal (Martin Rodger KC, Deputy Chamber President and Mr Peter D McCrea FRICS FCIArb) considered whether fitting out works undertaken at an office building should be valued by decapitalising the costs of the works at the statutory rate of 4.4%. The Tribunal concluded that the statutory rate should be used if the hereditament or part of it were being valued by means of the contractor’s basis of valuation but that its use was not mandatory in other costs based valuations. The Tribunal said at paragraph 105:

“Of course, the conclusion that the statutory rate is not mandatory does not mean that it cannot be used in an appropriate case. There is nothing to prevent the Tribunal or the parties from adopting that rate if it is considered appropriate to do so on the evidence. If there is no convincing evidence to help identify a more appropriate rate, the fact that the statutory rate is approved by Parliament and is required in certain valuations are both reasons why the Tribunal may be driven to adopt it rather than speculate about a rate of its own.”

48. In this case I have no evidence of decapitalisation rates other than the statutory one and it is that rate that I shall adopt. This means that in this case a standard 20ft container has an annual value of £71.90.

Issue 4: Should there be an allowance for the sloping nature of the site and if so, what would be an appropriate figure?

49. The final area of disagreement between the parties related to the allowance for the sloping nature of the site, Mr Bhatti having adopted 2.5% and Mr Rabbette 5%. Mr Rabbette had identified what he considered to be a comparable site in Northfield, Birmingham which was used as a yard for the retailing of timber and timber products. The assessment for this property contained a 5% end allowance for the sloping site. Photographs taken by Mr Rabbette showed the site to contain several timber sheds and canopies together with a shingle surface. A change in levels is clearly visible but Mr Rabbette did not provide any information about the size of the site or the gradient although he did say that the Property was more severely impacted as it had a distinct step and that vehicular access had been resolved by means of ramps. Mr Rabbette had sought an allowance of 10% at the VTE hearing but asked the Tribunal to adopt the 5% allowance used by the VTE in their determination. In the absence of any evidence from the appellant I will accept Mr Rabbette’s submission on this point.

Conclusion and determination

50. The valuation of the Property is therefore as follows:

|

|

Units/m2 |

Rate per unit/m2 |

Total |

|

|

|

|

|

|

Site |

1,453.75 |

£ 10.00 |

£ 14,538 |

| | | |

|

Containers (in terms of a 20ft unit) |

49 |

71.90 |

£ 3,523 |

| | |

|

| |

Sub total |

£ 18,061 |

| | | |

|

Less for sloping site |

-5% |

-£ 903 |

| | |

|

| |

Total |

£ 17,158 |

| | | |

| |

Say |

£ 17,100 |

51. The assessment is determined at rateable value £17,100 with effect from 8 April 2017.

52. The appeal was heard under the Tribunal’s simplified procedure under which costs are not normally awarded unless either party has behaved unreasonably, or the circumstances are in some other respect exceptional. I do not consider that either party acted unreasonably or that there are any such exceptional circumstances. I therefore make no order as to costs.

Mark Higgin FRICS FIRRV

Member

18 April 2023

Right of appeal

Any party has a right of appeal to the Court of Appeal on any point of law arising from this decision. The right of appeal may be exercised only with permission. An application for permission to appeal to the Court of Appeal must be sent or delivered to the Tribunal so that it is received within 1 month after the date on which this decision is sent to the parties (unless an application for costs is made within 14 days of the decision being sent to the parties, in which case an application for permission to appeal must be made within 1 month of the date on which the Tribunal’s decision on costs is sent to the parties). An application for permission to appeal must identify the decision of the Tribunal to which it relates, identify the alleged error or errors of law in the decision, and state the result the party making the application is seeking. If the Tribunal refuses permission to appeal a further application may then be made to the Court of Appeal for permission.