DECISION

Introduction

1. This is an appeal by the appellant, Intelligent Money Limited (“IML”), against a decision of the First-tier Tribunal (the “FTT”) dated 5 May 2022 with neutral citation [2022] UKFTT 338 (TC) (the “FTT Decision”) dismissing a claim by IML for repayment of VAT overpaid. The respondents are the Commissioners for His Majesty’s Revenue and Customs (“HMRC”).

2. The appeal concerns the liability to VAT of services provided by IML in connection with the provision, operation and administration of self-invested personal pension schemes (“SIPPs”), and, in particular whether those supplies fall within the exemption from VAT for “insurance and reinsurance transactions” contained in item 1 Group 2 Schedule 9 to the Value Added Tax Act 1994 (“VATA”).

3. Item 1 Group 2 Schedule 9 VATA implements article 135(1)(a) of Council Directive 2006/112/EC (referred to as the “Principal VAT Directive” (“PVD”)), which provides for the exemption of “insurance and reinsurance transactions, including related services performed by insurance brokers and insurance agents”. It is no part of either party’s case that the provisions of Group 2 Schedule 9 VATA do not properly implement article 135(1)(a) PVD. We have referred to the exemption from VAT provided by item 1 Group 2 Schedule 9 VATA and article 135(1)(a) PVD as the “insurance exemption” in this decision.

4. The FTT decided that the services provided by IML did not fall within the insurance exemption and dismissed IML’s appeal. IML appeals to this tribunal with the permission of the FTT.

The facts

5. The facts are not in dispute. They were set out by the FTT at paragraphs [7] to [36] of the FTT Decision. We gratefully adopt the FTT’s summary, which we have set out below.

The Intelligent Money SIPP

7. The contractual documentation which must be considered to determine the nature and liability of the supplies made by the Appellant consists of:

(1) An application form completed by a prospective member of the scheme

(2) A fee schedule

(3) The terms and conditions of the scheme

(4) The key features document (required to be provided under the regulatory provisions governing the provision of pensions)

(5) The trust deed and rules of the SIPP

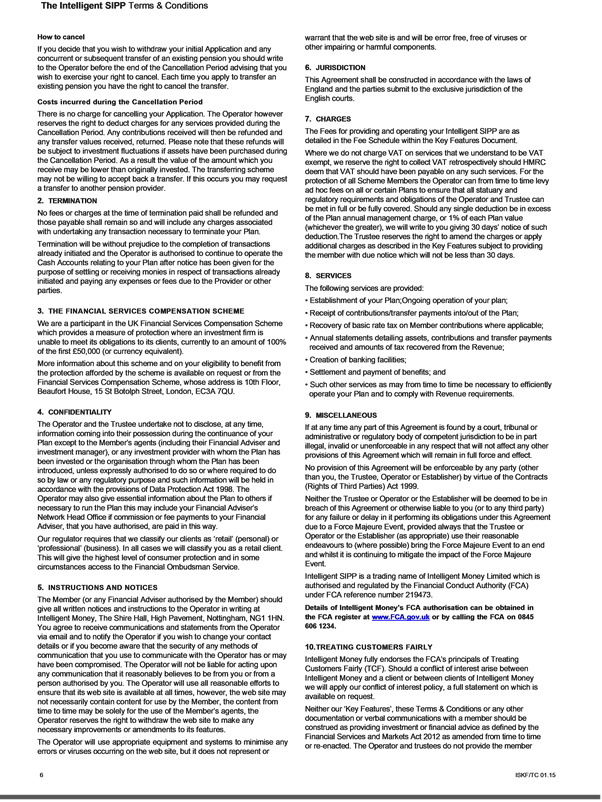

8. A copy of the composite document comprising the first 4 contractual documents is annexed to this judgment.

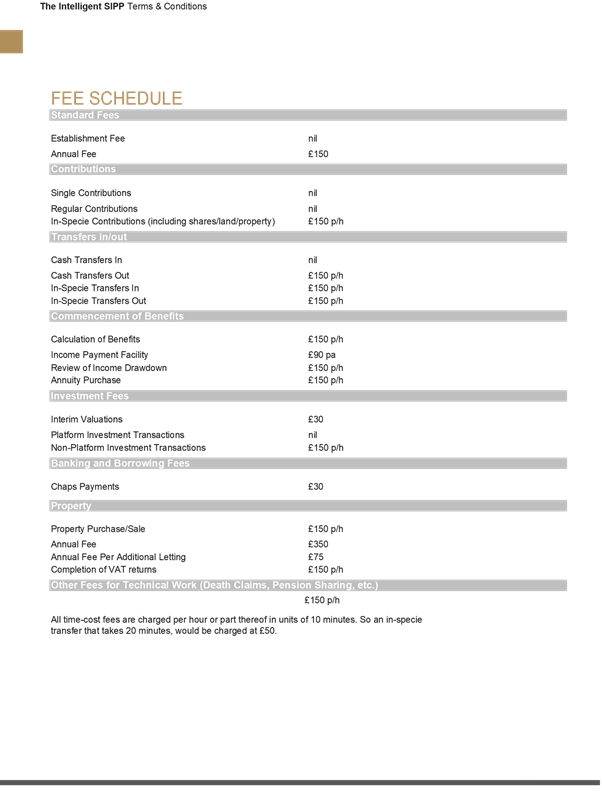

9. The parties took the Tribunal to the provisions of these documents at considerable length. The Tribunal has carefully considered all the terms referenced by each of the parties. However, for the purposes of this judgment the Tribunal does not propose to quote from the documents at length.

10. At the outset it is to be noted that the defining characteristic of a SIPP, including that offered by the Appellant, is that the contractual holder/their financial advisor (and not the Appellant) is responsible for the management of the funds held in the member's SIPP.

11. It is also significant that the SIPP is established so as to meet the detailed and specific requirements of the Finance Act 2004 (“FA 2004”), pursuant to which members may, subject to those requirements, save for their retirement in a tax efficient manner. Further detailed rules are imposed on the operation of the SIPP pursuant to the Pensions Act 2008 (“PA 2008”) . The rules place particular limits on when and how payments can be made from the SIPP to either the member or other beneficiaries. There are also certain restrictions on the level of contributions which can be made to the SIPP in respect of which tax relief can be claimed. The detail of these requirements is not relevant to the issue to be determined in this appeal. The Appellant's commitment to the investing members that the SIPP will be managed so as to preserve the tax effective status of the regime is, however, highly relevant.

Application form

12. An individual who wants to apply to become a member of the IM SIPP will complete the application form and provide their personal details together with what is referred to as an expression of wish as to "those people that [they] would like to receive any remaining benefits payable under the Intelligent SIPP on [their] death". It is noted that "This agreement does not bind the trustees of the scheme but is a means to help the trustees pay out [the] benefits in line with [the member's] wishes". The applicant warrants that they understand the non-binding nature of the expression of wishes in the declaration section.

13. Much of the detail requested to be provided ensures that the applicant is eligible for tax relief on contributions proposed to be made to the SIPP and ensure that the pension provided meets the requirements of FA 2004.

14. The application form includes a number of declarations (again many driven by the requirements of either the PA 2008 or FA 2004) including a declaration which has the contractual effect of incorporating the terms and conditions, fee schedule and deed and scheme rules such that the applicant (who becomes a member of the IM SIPP) is bound by their terms.

15. The applicant also declares that they are solely responsible for all decisions relating to the purchase, retention and sale of all investments within the SIPP and that the value of the SIPP may only be applied to provide benefits in accordance with the scheme rules.

Fee schedule

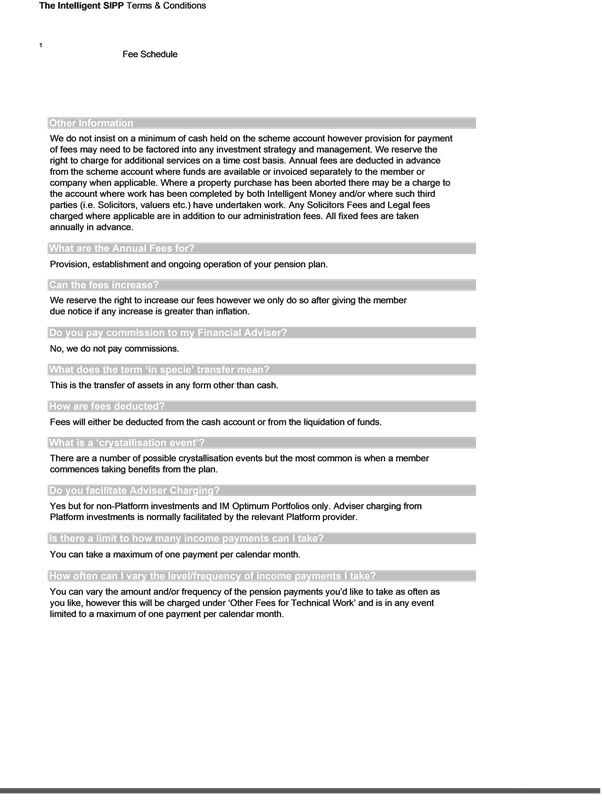

16. The fee schedule provides for specific fees to be payable. Every member is required to pay an annual fee of £150. Further fees are payable for instance where the member wishes to make an in-specie contribution/transfer, transfers out, on the commencement of payment of benefits, interim valuations, non-platform investment transactions, banking fees and in respect of property transactions. The majority of these latter fees are charged per hour.

17. Annual fees are stated to be for the "provision, establishment and ongoing operation of [the member's] pension plan". Annual fees are payable in advance and may be met from the member's cash account or from the liquidation of funds within the SIPP.

Terms and conditions

18. The key provisions of the terms and conditions are:

(1) Clause 1 provides the definitions.

(2) Clause 2 sets out that the agreement is between the Appellant and the member and that the SIPP has been established and will be operated so as to comply with the provisions of FA 2004 and that it is governed by a declaration of trust and rules pursuant to which the trustee is the legal owner of all investments which are held on behalf of the member and/or other beneficiaries of the member.

(3) Clause 3 sets out the provisions regarding contributions.

(4) Clause 5 outlines the operation of the member's cash account. Initially all contributions (and any associated tax relief) are paid into a cash account held on behalf of the member from which the member may then instruct how investments are made.

(5) Clause 7 concerns investments. The member is notified that there are a wide range of investments to which funds may be applied. The range of funds is stated to be restricted so as to ensure they remain compliant for the purposes of remaining within the FA 2004 tax efficient regime. The member or his financial advisor must select appropriate investments from the list provided.

(6) Investment procedures are set out in clause 8 - the member/their financial advisor selects appropriate investments which are then acquired by the trustee. The member is again reminded that the Appellant is not liable for any loss arising from the member's choice of investment. The Appellant preserves the right to sell investments for the purposes of paying benefits fees and charges under the plan.

(7) Pursuant to clause 10 the member has no right to vary the terms of the agreement.

(8) The member has a right to cancel under clause 11; they are, however notified that any refund in respect of investments made during the statutory cancellation period of 30 days will be subject to investment fluctuation and the sums refunded will be net of charges incurred.

(9) Clause 12 regarding termination provides that fees paid prior to termination are not refundable.

(10) Clause 17 concerns charges referencing the fee schedule.

(11) Clause 18 provides that the following services are provided:

"Establishment of your Plan;

- Ongoing operation of your plan;

- Receipt of contributions/transfer payments into/out of the Plan;

- Recovery of basic rate tax on Member contributions where applicable;

- Annual statements detailing assets, contributions and transfer payments received and amounts of tax recovered from the Revenue;

- Creation of banking facilities;

- Settlement and payment of benefits; and

- Such other services as may from time to time be necessary to efficiently operate your Plan and to comply with Revenue requirements."

(12) Under clause 20, Treating Customers Fairly, it is again reiterated that the Appellant does not provide financial advice to the member.

Key features

19. The key features document explains that the SIPP is a personal pension plan established under trust and approved by HMRC.

20. As with all other documents it repeatedly explains that the member is responsible for the suitability of investments requested to be made on their behalf by the trustee.

21. The aims of the SIPP are set out and essentially seek to provide the member with a tax efficient means of saving for a pension over which they have control of the investments made.

22. The member is reminded:

"A pension is a long-term investment for your retirement and benefits cannot normally be taken until you have reached your 55th birthday except in limited circumstances e.g. when you retire due to ill health, … There are also restrictions on the type and amount of benefits you can take from your Intelligent SIPP."

23. In connection with risk the member is provided with considerable detail as to the risks that they will bear if selecting to invest under the SIPP and reminded that they bear the risk of investment performance and as to decisions taken regarding the nature and timing of benefits taken.

24. Consistently with the terms and conditions the member is notified that all cash payments and transfers are paid into the cash account held on their behalf by the trustee from which investment instructions will be executed.

25. A full list of the tax compliant choices available to the applicant in respect of when and how to take benefits from the SIPP including by way of lump sum, taking a regular income or purchasing an annuity is set out.

26. Under a heading "what happens when I die?" the member is informed:

"When you join the Intelligent SIPP, you will complete an expression of wish form which allows the trustees … to pay benefits to your Nominees when you die.

The trustees will use an 'expression of wish' form to guide them in their decision as to how to pay this benefit, but this form is not binding upon them. This 'discretionary trust' structure means the payment can be made free from inheritance tax (IHT).

…

27. In respect of death before or after 75 the member is informed that death prior to 75 and prior to the taking of any benefits means that "the full value of your fund can be used to provide for your beneficiaries". Where benefits had been taken those benefits can be transferred to the successor or nominee.

Trust deed and rules

28. There were two sets of deed and rules in the bundle. The parties had prepared their cases by reference to different sets but agreed that there was no relevant difference between them. All references below are to the 2013 deed and rules as they were the relevant ones in the period covered by the claims to sums said to have been overpaid.

29. The SIPP is established under irrevocable master trust with the Appellant as the trustee. It is a registered pension scheme for the purposes of FA 2004 into which the individual or their employer may make contributions (see clause 3 of the deed). All contributions and/or transfers are held in identifiable member fund (clause 4). The sums so contributed are held within the trust and individually identifiable qua the member.

30. Clause 12 provides that the trustee may purchase an annuity on behalf of the member or other beneficiary and/or establish a policy of life assurance, they may also purchase units in unit trusts and insurer managed funds, purchase property and undertake any transaction permitted under FA 2004.

31. Pursuant to clause 13 the scheme may not make any payment representing an unauthorised payment under FA 2004 (in essence a payment in breach of the tax regime).

32. All investment transactions undertaken are required to be exercised "only in accordance with any directions given by the member" subject to ensuring compliance with FA 2004.

33. Clause 20 provides that "all costs, fees, expenses … in connection with the administration, management and investment of the Scheme may, subject to the agreement of the Scheme Administrator and the Scheme Trustee, … be paid directly to the Scheme Administrator or Scheme Trustee by the Member or may be paid on any other basis which the Scheme Administrator and Scheme Trustee agree. Otherwise, such amounts shall be paid by the Scheme Administrator out of the Member Fund or other asset of the Scheme in respect of which the amounts have been incurred …"

34. Rule 4 concerns contributions and provides that all contributions and their proceeds must be used to provide benefits in accordance with the rules. There is also provision for contributions to be used to purchase a life assurance contract (as one of the assets held) the proceeds of which may then be distributed as a benefit.

35. The commencement date for the payment of benefits is provided for in rule 5 and, consistently with the limitations provided for in order to be a registered pension scheme for tax purposes, benefits are payable from age 75 subject to an election to take them any time after the age of 55 though from an earlier date in the event of incapacity through ill health prior to attaining the age of 55.

36. The benefits arising under the scheme are particularised in clauses 6 - 8 which provide for member benefits: payment of a lump sum (as provided for/limited by section 164 FA 2004 ), an annuity (provided by an independent insurance company) and income from the assets; dependent pensions (which again may take the form of an annuity provided by an independent insurer); and death benefits in the form of a series of defined lump sum payments equal to the value of the fund at the time of the member's death as the trustee thinks fit having taken into consideration the member's expression of wish.

The FTT Decision

6. Having set out the facts, the FTT referred to the legislative background including: article 135(1)(a) PVD, Group 2 Schedule 9 VATA, Council Directive 2009/138/EC (the “Solvency II Directive”), the Financial Services and Markets Act 2000 (Regulated Activities) Order 2001, the Pensions Act 2008 and the Finance Act 2004.

7. The FTT then embarked upon a summary of the relevant case law. It began with the UK case law concerning the meaning of “insurance” in various contexts. In this respect, the FTT referred to the cases of Prudential Insurance Co v. Inland Revenue Commissioners [1904] 2 KB 658 (“Prudential”), a stamp duty case, and Fuji Finance Inc. v. Aetna Life Insurance Co. Limited [1997] Ch 173 (“Fuji”), on the application of the Life Assurance Act 1774, as well as the cases of Gould v. Curtis [1913] 3 KB 84 (“Gould”) and Medical Defence Union v. Department of Trade [1980] Ch 82 (FTT [43]-[55]).

8. In the course of that review, the FTT identified the key features of an insurance contract as set out by Channell J in Prudential (at p663) as being:

(i) a contract whereby, for some consideration, the insured secures some benefit, usually but not necessarily, the payment of money, upon the happening of some event;

(ii) the event must involve some amount of uncertainty, either that the event will ever happen or at the time at which it will happen;

(iii) the event must be adverse to the interest of the insured such that the payment meets some loss or other detriment on the happening of the event i.e. there must be an insurable interest in the subject matter (otherwise the contract is one of wager);

(iv) in the case of life insurance, the interest is not the measure of loss.

(FTT [44])

9. The FTT noted the developments in that test most notably, in Gould, where the Court of Appeal found that, whilst an adverse event is commonly present in the context of insurance, an insurable interest may be established without the requirement of adversity particularly in the case of “contingency insurance” which provides for a payment on the occurrence a contingent event (as opposed to “indemnity insurance” which provides an indemnity against loss) (FTT [46]); and, in Fuji, where the Court of Appeal held that a short-term investment contract, under which a sum calculated by reference to the price of units currently allocated to the policy was payable on the death of the life assured or on its earlier surrender, was a contract of life insurance because the necessary requirement of “uncertainty” was present in that the timing of each of the potential circumstances in which a benefit was payable was uncertain (FTT [53]).

10. We have referred to the test in Prudential as developed through the UK case law as the “Prudential test” in the remainder of this decision notice.

11. The FTT also reviewed the case law relating to the VAT exemption, beginning with the VAT & Duties Tribunal case of Winterthur Life UK Limited v. Customs & Excise Commissioners [1997] Lexis Citation 1166 (“Winterthur”) before turning to the decisions of the Court of Justice of the European Union (and its predecessor the European Court of Justice) (“CJEU”) on the meaning of “insurance transactions” for the purposes of article 135(1)(a) PVD (and its predecessor article 13(B)(a) of Council Directive 77/338/EEC or the “Sixth Directive”) being Card Protection Plan Limited v. Customs & Excise Commissioners (Case C-349/96) (“CPP”), Directeur General des Finances Publiques v. Mapfre (Case C-584/13) (“Mapfre”), Minister Finansow v. Aspiro SA (Case C-40/15) (“Aspiro”), and United Biscuits (Pension Trustees) Limited v. HMRC (Case C-235/19) (“United Biscuits”) (FTT [56]-[82]).

12. We will return to this case law later in this decision notice. For present purposes, it is sufficient to note that the FTT identified that the criteria for a transaction to be treated as an “insurance transaction” for the purposes of the insurance exemption are consistently stated in the CJEU case law as being “that the insurer undertakes in return for prior payment of the premium, to provide the insured, in the event of materialization of the risk covered, with a service agreed when the contract was concluded” (FTT [78], citing the CJEU decision in United Biscuits [30]).

13. Having set out the parties’ submissions in some detail, the FTT addressed the question of whether or not the SIPP operated by IML (the “IM SIPP”) was a contract of insurance for the purpose of the Prudential test. It dealt with this issue first, before addressing whether or not the provision of the IM SIPP should be regarded as an “insurance transaction” for VAT purposes for two reasons:

(1) first, the statements in HMRC’s manuals (in particular, VATINS2110 when taken together with the comments at GIM1040) implied that the provision of a life insurance contract meeting the Prudential test would be treated as an insurance transaction for VAT purposes; and

(2) second, IML’s case before the FTT was that the UK case law, principally Prudential and Fuji, was determinative of the issue and so, if the contract was not a contract of insurance applying the Prudential test, there was no further issue for the tribunal.

14. The FTT concluded that the IM SIPP was a contract of insurance within the Prudential test. In summary, this was on the basis that no relevant distinction could be made between the arrangements in Fuji and the IM SIPP. In particular, no distinction should be made on the grounds that the premiums became legally and beneficially owned by the insurance company, in the Fuji case, whereas the contributions were held under the trust arrangements, in the case of the IM SIPP, and so remained “substantively the members’ own funds” (FTT [118]-[120]).

15. The FTT then turned to the question of whether the IM SIPP was an insurance transaction for the purposes of the insurance exemption. It undertook its analysis by reference to whether or not there was a material difference between the test as set out in the CJEU case law and the Prudential test.

16. The FTT’s reasoning was, in summary, as follows:

(1) The justification for the insurance exemption was that it was intended to address the difficulties arising from the fact that “an insurance premium comprises two parts: the fee for administration/provision of the policy under which the insured risk is borne and the capital element (from which claims are ultimately paid)” (FTT [130], citing the decision of the CJEU in United Biscuits). That purpose was fundamentally different from the purpose of the Prudential test, which was primarily developed for regulatory reasons (FTT [128]).

(2) On that basis, a supply was exempt from VAT under the insurance exemption “where in return for a fixed and known amount the insurer agrees to provide benefits on the materialization of an identified risk where the scope of the benefits is specified at the outset” (FTT [131]).

(3) Notwithstanding IML’s arguments (based on the domestic non-VAT case law) that the assumption of risk by the insurer was not a relevant characteristic of an insurance contract, in the CJEU case law, the assumption of risk by the insurer did “appear to be significant” (FTT [133]). The FTT justified this conclusion by reference to the decisions of the CJEU in Aspiro, Mapfre, and United Biscuits. The FTT says this (at FTT [134]-[136]):

134 The Advocate General in Aspiro analysed the essential features of an insurance transaction by reference to the assumption of risk by the insurer (at paragraph [22]). At paragraph [26] and by reference to the CJEU judgments in Försäkringsaktiebolaget Skandia (publ), C-240/99 and Assurandør-Societetet, acting on behalf of Taksatorringen v Skatteministeriet C-8/01 the Advocate General draws a distinction between insurance transactions in a "strict sense" and component elements of insurance business confirming that it is the assumption of risk by the insurer which is critical for an insurance transaction in a VAT sense.

135 In paragraph [42] of Mapfre the CJEU specifically articulates the essential features of an insurance transaction by reference to the insured person being exempted from the risk of bearing financial loss, which is uncertain, but potentially significant.

136 The "insurance in the strict sense" distinction is picked up by the Advocate General in United Biscuits at paragraph [68] in which it is noted that the PVD exempts insurance business "in the strict sense of the term, in that such an activity involves solely the assumption of risks in a contractual framework". The precise distinction is not articulated by the CJEU however, at paragraph [28] it references the requirement for indemnity and, where, at paragraph [40] the CJEU references the "normal meaning" of insurance the CJEU does so explicitly approving paragraph [58] of the Advocate General's opinion in which substantively the same distinction is drawn between "insurance" in the strict sense and "operations" which are closely related or ancillary to the provision of insurance.

(4) That position could be contrasted with the Prudential test. For a transaction to be an “insurance transaction” for VAT purposes, the insured must pay the insurer to assume a financial risk, whereas that was not a requirement of the Prudential test. The result was that some life assurance policies which met the Prudential test for an insurance contract would fall outside the scope of the insurance exemption. The FTT says this at FTT [137]:

137 It appears to the Tribunal that what is required under the Prudential test is somewhat different to that which is relevant for the purposes of the VAT exemption. In order for a supply to be exempt as an insurance transaction, the insured must pay the insurer to assume a financial risk. Such a conclusion includes within the scope of the exemption both indemnity and contingency insurance as, under a conventional (non-investment) life assurance policy the insured pays a fixed, up-front, annual or monthly premium over the term of the policy and the insurer bears the risk on a fixed sum payment on the happening of the insured event (death/critical illness etc). However, excluded from exemption is any policy/scheme which meets the Prudential life/death uncertainty without the assumption of financial risk.

(5) This scope is consistent with the rationale for the insurance exemption (FTT [138]). The scope of the EU insurance directives was not a relevant factor (FTT [139]-[140]).

(6) The fees paid by participants in the IM SIPP were paid as consideration for services. They did not include any premium for risk. IML did not provide insurance “in the strict sense” because it did not assume any financial risk. The FTT concludes as follows (at FTT [141]):

141 The annual fees payable by a member of the IM SIPP are paid as consideration for the provision of the services listed in clause 18 of the terms and conditions. They do not include any element of risk premium and the Appellant does not need to accumulate capital from which to pay the benefits. The members contributions which are held under trust for the member, their dependents and other beneficiaries, represent the capital from which the benefits are paid. The Appellant does not provide insurance in the “strict sense” of assumption of financial risk rather, it has established and operates a trust scheme pursuant to which contributions made by the members are held and administered so as to comply with the provisions of [the Finance Act 2004].

17. On that basis, the FTT decided that the fees payable by the members of the IM SIPP were not consideration for an exempt “insurance transaction” and dismissed IML’s claims for repayment of overpaid tax (FTT [145]).

18. The FTT accepted that its decision was contrary to the decision of the VAT & Duties Tribunal in Winterthur (FTT [143]). We will return to the decision in that case and the other case law later in this decision.

Grounds of appeal

19. The FTT granted IML permission to appeal on four grounds. They were, in summary:

(1) that the FTT erred in its interpretation of the CJEU decision in United Biscuits in concluding that the lack of investment risk in the transactions between IML and the members of the IML SIPP was determinative of the appeal;

(2) that the FTT erred in its interpretation of the earlier CJEU cases (CPP, Aspiro and Mapfre) in concluding that the CJEU decisions limited the exemption for insurance transactions to indemnity insurance as opposed to contingency insurance;

(3) that the FTT erred in failing to appreciate that it is a consequence of its analysis that the type of life insurance policies with an investment element, such as those in issue in Fuji, cannot benefit from VAT exemption;

(4) that the FTT erred in its analysis of Winterthur in taking the view that HMRC’s argument in that case was based solely on the fact that the charges in question were not paid to an insurance company.

20. Before us, Mr Bedenham acknowledged that the core issue underlying the first two grounds was whether the FTT erred in its interpretation of what constitutes an “insurance transaction” for the purpose of the insurance exemption, and thereby erred in finding that IML’s supplies did not fall within the exemption. Mr Bedenham also accepted that the third and fourth grounds were not standalone grounds of appeal, and the tribunal does not need to address them separately. We have proceeded on that basis.

The parties submissions in outline

21. We will address the parties’ submissions in greater detail in our discussion of the issues. However, it will assist our explanation if we first set out briefly the parties’ respective positions.

22. Mr Bedenham, for IML, makes the following points.

(1) There is no material distinction between criteria in the Prudential test for determining whether a transaction should be regarded as “insurance” as a matter of UK law and the criteria for determining whether a supply is an “insurance transaction” for VAT purposes (as derived from the CJEU case law).

(2) Having made the findings of fact that it did and, based on those facts, concluded that the IM SIPP met the criteria to be treated as an insurance contract under the Prudential test, the FTT should also have concluded that the supplies made by IML in relation to the IM SIPP were insurance transactions for VAT purposes (and so fell within the insurance exemption).

(3) All the essential features of an insurance transaction as required by the CJEU case law (CPP [17], United Biscuits [30]) are present: the insurer is defined by reference to the transaction, in this case IML; the annual fees and other charges paid in advance, and to an extent contributions to the funds, represent the premiums paid; under the arrangements, IML agreed to provide a service (i.e. the payment of the life and death benefits); that service was to be provided on the materialization of the risk covered, in this case, the trigger event for the payment of the benefits.

(4) The FTT fell into error by adding a criterion that the insurer must assume financial risk (FTT [137]). The addition of that criterion was not justified by the CJEU case law. The only requirement is a contingency. The relevant contingency in this case is the uncertainty of the event in relation to which benefits will be paid (as in Fuji).

(5) The effect of the FTT’s error is that some life insurance contracts - namely those linked to investment contracts - fall outside the exemption, when clearly they should be regarded as insurance contracts.

23. Mr Macnab, for HMRC, supports the conclusion of the FTT, but not of all of its reasoning. He makes the following points:

(1) The essential features of an insurance transaction for the purpose of the insurance exemption as established by the CJEU case law were correctly identified by the FTT (being those set out at [12] above).

(2) Those criteria require the “prior payment of a premium”. The members of the IM SIPP do not pay a premium. The contributions made by members are not consideration for any supply. The only payments made in advance are the annual fees. The annual fees are paid for a continuing service, namely the operation and management of the SIPP, and not for the provision of the benefits on the materialization of a risk. The other charges are for particular services and are paid at the time or after the service is provided.

(3) IML does not undertake to provide the life and death benefits under any relevant binding contractual obligation with the member of the IM SIPP. IML makes those payments as trustee of the fund from the member’s accumulated pension pot.

(4) The IM SIPP does not cover any “risk”. The FTT was correct in its interpretation of the case law. The requirement that an insurance transaction provides an indemnity from risk is simply a means of expressing the criterion in the case law that the insurer must provide a service “in the event of the materialization of the risk covered”. It is not an additional criterion.

(5) The FTT was wrong to conclude that the IM SIPP was a contract of insurance under the Prudential test. However, that issue is not relevant to the subject matter of this appeal.

Discussion

24. We have set out the terms of the insurance exemption in both article 135(1)(a) PVD and Group 2 Schedule 9 VATA at [2] and [3] above. There was no argument between the parties that the UK legislation did not properly implement the provisions of the PVD.

25. Both IML and HMRC agreed that the real issue in this appeal is what criteria have been set down by the CJEU for the purpose of the insurance exemption and whether the IM SIPP meets those criteria. We therefore propose to begin our discussion of the relevant principles by reference to the criteria established by the CJEU in its decisions. We will comment on the domestic case law later in this decision.

The CJEU case law

26. We will begin with the four key decisions of the CJEU concerning the interpretation of the insurance exemption, on which the FTT relied in its decision: CPP, Mapfre, Aspiro, and United Biscuits.

CPP

27. The first such case is CPP. In that case, CPP offered holders of credit cards, on payment of a certain sum, a plan intended to protect them against financial loss and inconvenience resulting from the loss or theft of their cards or of certain other items such as car keys, passports and insurance documents. In so far as the plan provided for compensation to the cardholder against financial loss in the event of loss or theft, CPP obtained block cover from an insurance company under a policy arranged by an insurance broker instructed by CPP.

28. At CPP [17], quoting from the Advocate General’s opinion, the CJEU set out the essential features of an “insurance transaction” in the following terms:

… the essentials of an insurance transaction are, as generally understood, that the insurer undertakes, in return for prior payment of a premium, to provide the insured, in the event of materialisation of the risk covered, with the service agreed when the contract was concluded.

29. These essential features are repeated consistently in the later cases (see Mapfre [28], Aspiro [22], United Biscuits [30]). The CJEU decided that the service provided by CPP to its customers was capable of meeting the essential requirements and so being treated as an “insurance transaction” within article 13(B)(a) of the Sixth Directive.

30. The other key points that we take from the CJEU’s decision in CPP are as follows.

(1) First, the CJEU noted (CPP [18]) that, for this purpose, it was not an essential requirement that the service the “insurer” undertook to provide for these purposes took the form of the payment of a sum of money. It might also take the form of the provision of a service.

(2) Second, the services provided by CPP fell within the definition even though CPP was not itself an insurance company and the risk was ultimately borne by the insurance company under the block policy. In the CJEU’s view, the concept of “insurance transactions” was broad enough “to include the provision of insurance cover by a taxable person who is not himself an insurer but, in the context of a block policy, procures such cover for his customers by making use of the supplies of an insurer who assumes the risk insured” (CPP [22]).

(3) The CJEU in CPP also took the view that there was “no reason” for the interpretation of the term “insurance” to differ from its meaning for the purpose of the EU directives on insurance (CPP [18]). The CJEU takes a different view on this point in the later cases (see our comments on United Biscuits below).

Mapfre

31. The next case to which we should refer is Mapfre. The case concerned the VAT treatment of warranties provided by Mapfre to purchasers of second-hand motor vehicles from certain dealers covering the repair of the vehicles in the case of mechanical breakdowns.

32. Having set out the essential features of an “insurance transaction” in similar terms to its decision in CPP [17] (Mapfre [28]), the CJEU records that:

… an insurance transaction necessarily implies the existence of a contractual relationship between the provider of the insurance service and the person whose risks are covered by the insurance, that is to say, the insured party… (Mapfre [29])

33. The CJEU found that the transaction in the Mapfre case was capable of meeting all the essential criteria of an “insurance transaction”. The CJEU says this at Mapfre [39]:

39 All of the characteristic elements of an insurance transaction, such as those identified by the case-law cited in paragraph 28 of the present judgment, exist in each of those situations. Thus, the insurer, which in this case is Mapfre warranty, is an economic operator independent of the second-hand-vehicle dealer and the insured person is the purchaser of that vehicle. Furthermore, the risk consists of the need for the purchaser of the second-hand vehicle to pay for the repairs in the event of a mechanical breakdown covered by the warranty, the cost of which the insurer undertakes to cover. Finally, the premium consists of the lump sum which the purchaser of the second-hand vehicle pays, either in the purchase price of that vehicle or as a supplement.

34. The CJEU also identified, at Mapfre [42], what it regarded as the essence of an “insurance transaction” - namely the payment of a premium by the insured person in return for the removal of the risk of bearing an uncertain financial loss - in the following terms:

42 In this regard, as the Advocate General has observed in point 28 of his Opinion and as is clear from the case-law cited in paragraph 28 of the present judgment, the essence of an 'insurance transaction', within the meaning of Article 13(B)(a) of the Sixth Directive, lies in the fact that the insured person is exempted from the risk of bearing financial loss, which is uncertain, but potentially significant, by the premium, payment of which for that person is certain but limited.

35. It is the above passage on which the FTT particularly relies in support of its conclusion that an “insurance transaction” must involve the exemption of the insured party from a risk of bearing financial loss.

Aspiro

36. The third case is Aspiro. That case involved a company, Aspiro, that supplied claims settlement services under contractual arrangements with insurance companies, without itself incurring any liability to the insured persons. The CJEU decided that, even if these services might form part of an insurance transaction, they did not fall to be treated as “insurance transactions” within the insurance exemption when separated from the related provision of insurance cover.

37. Before we turn to the decision of the CJEU in this case, we will refer first to various aspects of the opinion of the Advocate General, Advocate General Kokott.

38. Advocate General Kokott points out in her opinion that a contractual relationship between the provider of the insurance service and the insured person and the assumption of risk are essential elements of an insurance transaction. She says this at paragraph [22] of her opinion :

… The concept also encompasses the provision of insurance cover by a taxable person who is not himself an insurer but who procures such cover for his customers by making use of the services provided by an insurer. In other words, the relevant factor is assumption of risk in return for payment. It presupposes a contractual relationship between the provider of the insurance service and the insured party.

39. In this case, Aspiro did not undertake to cover risks nor was it in a contractual relationship with the insured person.

40. Furthermore, the insurance exemption could not extend to transactions, which might form part of an insurance transaction, but did not include the assumption of risk. She says this (Aspiro AG [26]):

… Article 135(1)(a) of the VAT directive does not, for example, refer generally to transactions in the insurance business or the management of insurance policies but, according to its wording, only to insurance transactions in the strict sense, as the court has repeatedly held. The assumption of risk, which, according to case law, is the sole constituent of an insurance transaction, cannot be broken down into separate services.

41. This is the first reference, in the cases to which we have been referred, to the concept of insurance “in the strict sense” to refer to a transaction that involves an assumption of risk (and to which the FTT refers at FTT [134] and FTT [136]).

42. The CJEU appears to follow this approach, but without reference to any concept of insurance “in the strict sense”. Having repeated the essentials of an insurance transaction as set out in CPP (Aspiro [22]), the CJEU says this (at Aspiro [23] and [24]):

23 … such transactions necessarily imply the existence of a contractual relationship between the provider of the insurance service and the person whose risks are covered by the insurance, that is to say, the insured party (see judgment in Taksatorringen, C-8/01, paragraphs 40 and 41).

24 However, in the present case, a provider of services such as Aspiro does not itself undertake to ensure that the insured person is covered in respect of a risk and is not connected in any way to the insured person through a contractual relationship.

United Biscuits

43. The final decision of the CJEU to which the FTT referred is United Biscuits. That case concerned the VAT treatment of investment management services provided to managers of pension funds by investment managers that were not insurance companies.

44. We should refer once again to the opinion of the Advocate General, in this case Advocate General Pikamae, as it features prominently in the FTT Decision.

(1) The Advocate General confirms that it is the assumption of risk that allows an activity to be classified as an “insurance transaction” and cites the passage from the CJEU decision in Mapfre (Mapfre [42]) concerning the essence of an insurance transaction as involving the insured person being protected from the risk of financial loss (United Biscuits AG [40]).

(2) Advocate General Pikamae refers (United Biscuits AG [41]) with approval to the passage from Advocate General Kokott’s opinion in Aspiro (to which we refer above) in which she refers to insurance “in the strict sense”, as authority for a restrictive interpretation of the insurance exemption that does not extend to related financial transactions.

(3) On that basis the Advocate General concludes that the investment management services provided to the pension fund managers were not within the scope of the insurance exemption.

(4) As regards the relevance of the EU insurance directives, those directives extended to both insurance transactions and, for regulatory reasons, related operations. Those related operations were not insurance transactions in the strict sense (United Biscuits AG [56]-[63]).

(5) By contrast, the reasons for the insurance exemption from VAT were twofold: first, to avoid the risk of double taxation of such transactions as a result of the ability of EU member states to levy taxes on insurance contracts being preserved by article 401 PVD; and second, to avoid the difficulties of determining in advance the taxable amount of premiums which would represent partly remuneration for the service provided by the insurer and partly a contribution to the capital required to cover risks as and when they materialized (United Biscuits AG [64]-[68], in particular AG [66] and footnote 54).

45. In its decision, the CJEU adopts this rationale and finds that the services provided under the contractual arrangements in United Biscuits were not insurance transactions. This was because the insurance exemption was justified by the difficulty of determining the correct amount of VAT on insurance premiums relating to the coverage of risk. The services in question were fund management services, which did not involve any element of protection from risk. The CJEU says this (at United Biscuits [31] and [32]):

31 In the present case, the referring court indicates, and this was confirmed at the hearing, that the services contractually provided to the applicants in the main proceedings consisted of fund management solely for their account, to the exclusion of any indemnity from risk.

32 It is common ground that such supplies of services do not meet the criteria referred to in paragraphs 29 and 30 of this judgment, since the exemption provided for in Article 135(1)(a) of Directive 2006/112 is, in essence, justified by the difficulty of determining the correct amount of VAT for insurance premiums relating to the coverage of risk.

46. No other relevant criteria relevant to the concept of “insurance transactions” could be derived from the CJEU case law regarding the meaning of “insurance” in the EU insurance directives. The previous decisions of the CJEU (including CPP [18]) should not be read as confirming that services treated as “insurance” within the EU insurance directives should be regarded as “insurance transactions” for the purpose of article 135(1)(a) PVD (United Biscuits [33]-[51]).

47. On that basis, the CJEU held that investment fund management services, which did not provide any indemnity from risk, could not be classified as “insurance transactions”, within the meaning of article 135(1)(a) PVD and so did not qualify for exemption (United Biscuits [52]).

Other CJEU decisions

48. We have also been referred by the parties to two more recent decisions of the CJEU: Q-GmbH v Finanzamt Z (Case C-907/19) (“Q-GmbH”) and Generali Seguros SA v Autoridade Tributaria e Aduaneira (Case C-42/22) (“Generali”). For the most part, these two cases confirm the principles derived from the earlier case law.

49. Q-GmbH concerned the VAT treatment of three types of supplies: (i) the development and supply of insurance products by Q-GmbH to an insurer, (ii) the placement of those insurance products for the insurer (where the insurance contract was then entered into between the insurer and the policyholder), and (iii) the management of insurance contracts and the settlement of claims. Having reiterated the principles established in other cases, the CJEU found that the supplies made by Q-GmbH did not fall within the insurance exemption because there was no contractual relationship to which it was a party under which risks of another party were covered. The CJEU says this (at Q-GmbH [33]):

33 Thus, it is clear that the service provided by Q, consisting of the grant of a licence for the use of an insurance product, cannot be classified as an insurance transaction, as the grantor is contractually linked only to the insurer who uses the product in question in accordance with the licence agreement. According to the referring court, Q is also not responsible for covering the risks insured on the basis of that product.

50. Generali concerned the purchase by an insurance company from its motor insurance customers of parts from motor vehicles that had been written-off and the sale of those parts by the insurance company. The CJEU reiterated the objective of the insurance exemption (Generali [32]) and the essential features of an insurance transaction (Generali [33]) from the earlier cases. It found that these transactions did not fall within the insurance exemption because even though the transactions were undertaken by the insurance company they were under separate arrangements from the provision of insurance. The CJEU says this (at Generali [35]-[37]):

35 It should be noted that transactions for the sale of parts from written-off motor vehicles, such as those at issue in the main proceedings, take place under agreements separate from the insurance contracts covering those vehicles, those agreements being concluded by the insurance undertaking with persons other than the persons insured and not being covered by an insurance relationship.

36 The sale of goods bears no relation to covering a risk and the price corresponds to the value of the goods concerned at the time of that sale. The determination of the basis of assessment for VAT does not involve any difficulty in such a case.

37 The fact that, as was pointed out in paragraph 27 of this judgment, such a transaction relates to parts from a written-off motor vehicle that was involved in an accident covered by the insurance undertaking which is selling it and that the amount of the compensation due to the person insured as a result of that accident includes the purchase price of those written-off parts is irrelevant in that regard. The value of the parts constitutes the residual value, after the accident, of the insured vehicle and is therefore not, by definition, part of the damage suffered by the insured person. Consequently, that price does not form part of the insurance compensation itself, and is paid to the insured person under a contract of sale separate from the insurance agreement and separable from it.

51. The decision in Generali was issued after IP completion day (as defined for the purposes of the European Union (Withdrawal) Act 2018) and so is not binding upon this tribunal. However, the tribunal may have regard to the decision so far as it is relevant to the matters before tribunal.

Principles derived from the CJEU case law

52. The principles that we derive from our review of the CJEU case law are, in summary, as follows:

(1) The essential features of an insurance transaction are consistently stated by the CJEU to be that the insurer undertakes, in return for prior payment of a premium, to provide the insured, in the event of the materialization of the risk covered, with the service agreed when the contract was concluded (CPP [17], Mapfre [28], Aspiro [22], United Biscuits [30]).

(2) An insurance transaction does not require the payment of cash by the insurer when the risk materializes. The essential requirements can be satisfied in cases where the provider of the insurance service provides a service on the materialization of the risk (CPP [18]).

(3) Those essential features imply the existence of a contractual relationship between the provider of the insurance service and the person whose risks are covered by the insurance, i.e. the insured party (Mapfre [29], Aspiro [23]).

(4) Under that contractual relationship, the insured party must obtain some protection or coverage from risk (United Biscuits [31]). The meaning of “risk” in this context is one of the central issues in this case to which we will return. We note for present purposes that none of the CJEU cases involves the provision of life insurance.

(5) The rationale for the exemption is to be found, at least in part, in the difficulty of determining the taxable amount of premiums which represent partly remuneration for the coverage of risk and partly a contribution to the capital required to cover risks (United Biscuits AG [66] and footnote 54, United Biscuits [32]).

(6) Exemptions from VAT should be read strictly (see, for example, United Biscuits [29]). The exemption in article 135(1)(a) PVD does not extend to “insurance business” (i.e. other things that insurers commonly do). It is limited to transactions involving the coverage of risk i.e. to transactions involving insurance “in the strict sense” (Aspiro AG [26], United Biscuits AG [41] and AG [68]).

(7) It does not matter whether, under the arrangements as a whole, the provider of the insurance service to the insured party ultimately bears the risk from which the insured party is protected or whether that risk is assumed by a third person. The concept of an insurance transaction can include the provision of insurance cover by a person, who is not an insurer, but who procures cover for customers by making use of the supplies of an insurer who assumes the risk (CPP [22], Aspiro AG [22]).

(8) The definition of an “insurance transaction” for the purposes of the insurance exemption is not informed by the meaning of “insurance” for the purposes of the EU insurance directives (United Biscuits [33]).

The domestic case law

53. As we have mentioned above, to some extent, Mr Bedenham relies on domestic non-VAT case law in support of his position. He does not dispute that, in determining whether a supply is an “insurance transaction” within the insurance exemption, the decisions of the CJEU must be applied. There is ample authority to support the view that the exemptions from VAT contained within the PVD contain autonomous concepts of EU law which must be given a consistent meaning (see for example CPP [15]).

54. On that basis, the decisions of domestic courts on the meaning of “insurance” outside the context of the insurance exemption from VAT are strictly not relevant. However, Mr Bedenham says that reference to the domestic case law can be instructive and assist the interpretation of the relevant VAT provisions. Furthermore, he says, the factors that have to be taken into account in determining whether a supply is an “insurance transaction” for the purpose of the insurance exemption are essentially the same as those that apply when determining whether a contract is, as a matter of domestic law, a contract of insurance.

55. We have set out above, in our summary of the FTT Decision, the facts and key points arising from the Prudential case. In that case, Channell J identified the criteria for determining whether the given contract was a contract of insurance for stamp duty purposes. Those criteria formed the basis of the Prudential test. They were expanded upon by the Court of Appeal in Gould, where the Court of Appeal decided that an insurance contract could encompass provision for payment on an uncertain contingent event and did not require the event to be adverse to the insured person.

56. The next case to which we should refer is Fuji. Once again, we have set out the facts briefly above, but, in summary, the case concerned the treatment of a capital investment bond under the terms of which the amount subscribed was notionally allocated to certain investment funds and life and death benefits were payable by reference to the value of the units in the funds. The allocation of the subscription price to the funds was, however, only notional; the funds remained the property of the life insurance company. On that basis, the Court of Appeal found that the investment bond was a form of life insurance. Morritt LJ - relying on the decisions of the Court of Appeal in New Zealand in Marac Life Assurance Limited v Commissioner of Inland Revenue [1986] 1 NZLR 694 and the Federal Court of Australia in N M Superannuation Pty Limited v Young 113 ALR 39 - found that there was sufficient uncertainty in the payment under the contract for the contract to be regarded as one of life insurance as the payments were contingent upon death, the timing of which was uncertain, or reaching a given age, the attainment of which was uncertain (p185E - p186C, p186H - p187F). It did not matter that the insurer was not exposed to any financial risk (p189B). Hobhouse LJ agreed (p198C-F).

57. The decisions in Prudential and Fuji were not made in the context of the insurance exemption from VAT. The one domestic decision to which we have been referred in relation to the insurance exemption is Winterthur. This was a case before the VAT & Duties Tribunal. The case concerned the payment of fund management fees charged by two subsidiaries of a life insurance company, which acted as the trustee of two pension schemes under which the members of the schemes had control and management of the funds representing their and their employers’ contributions.

58. The tribunal found that the schemes were capable of being treated as life insurance contracts by reference to the Court of Appeal decision in Fuji to which we have referred above, and, on that basis, the payment of the management fees fell within the insurance exemption. In doing so, the tribunal dismissed an argument on behalf of HMRC that there was no contract of insurance between the members and the life company to provide the relevant benefits. The tribunal reached this conclusion on the basis that the arrangement as a whole could be read as importing that obligation.

59. The tribunal also found that contributions paid by the members to the funds could be regarded as consideration paid for the benefits provided under the scheme even though, for the most part, the contributions were made to a fund held on behalf of the member and his or her dependents. The tribunal justified this conclusion on the grounds that the contributions could also be used to pay the administrative expenses of the scheme. The tribunal said this:

As a refinement of his contract point Mr Vajda objected that the moneys contributed by the member to the Scheme were not consideration for the benefits payable under the Scheme, since those moneys were impressed with a trust for the member and his dependants. This proposition seems to me to be only partly true. The funds contributed by the member, besides being impressed with the trusts mentioned above, are also charged with the payment of the administrative expenses of the Scheme (so far as those expenses are not paid directly by the member), so that there is an element of monetary consideration moving from the member: the fact that this consideration is relatively small by comparison with the member's total contributions cannot, it seems to me, prejudice the insurance status of the Scheme, if (as the authorities indicate) it is unnecessary for the insurance to involve any element of risk on the part of the insurer. The consideration which a risk-free insurer receives may well be relatively small in comparison with the moneys paid out under the insurance.

Application to the facts of this case

60. The parties agree that the relevant criteria for determining whether the arrangements in this case involve “insurance transactions” are those set out by the CJEU in CPP and the other cases to which we have referred. For ease of reference, those essential features are that the insurer undertakes, in return for prior payment of a premium, to provide the insured, in the event of the materialization of the risk covered, with the service agreed when the contract was concluded. There are no other relevant criteria.

61. We have heard submissions from the parties on various specific aspects of this definition including: whether the arrangements involve the prior payment of a premium; whether the insurer (IML) undertakes to provide the member with a relevant service agreed when the contract was concluded; and whether the arrangements involve the materialization of a risk. However, the central issue between the parties is whether it is implicit in this definition that the insurer will assume an element of risk and, if so, what is the nature of “risk” in this context. That issue encompasses many of the more detailed submissions that have been made by the parties and so we will address it first, before commenting on two specific aspects, whether the arrangements involve the prior payment of a premium, and the nature of the service provided by IML under the arrangements.

The assumption of risk

62. As we have mentioned in our summary of the case law above, the CJEU consistently refers to an insurance transaction as involving the assumption of risk or the coverage of risk (see [52(4)] above). This requirement is expressed in various ways, for example, the CJEU refers in some cases to the insured person being “exempted” from risk (for example, Mapfre [42]) or the insured person being provided with an “indemnity from risk” (United Biscuits [31]) or the insured person being “covered” in respect of a risk (Aspiro [24]). The references in the opinions of the Advocates General in Aspiro and United Biscuits to insurance “in the strict sense” are coupled with references to the “assumption of risk” as being the essence of an insurance transaction that falls within the insurance exemption (Aspiro AG [26], United Biscuits AG [41], and AG [68]).

63. Some of the references in the CJEU case law might be regarded as going further in suggesting that an insurance transaction must involve protection against a risk of bearing “financial loss”. These references appear, for example, in the CJEU decision in Mapfre (Mapfre [42]), which is cited in the Advocate General’s opinion in United Biscuits (United Biscuits AG [40]). This requirement does not, however, consistently appear - it is not, for example, repeated in the CJEU decision in United Biscuits - and, in Mapfre, the limitation did not have any bearing on the outcome of the case.

64. The FTT concluded that the effect of the CJEU decisions was that it was a requirement of an insurance transaction that the insurer must assume a financial risk (FTT [137]). Mr Bedenham submits that that conclusion was wrong. He says that the assumption of risk by the insurer is not an essential feature of an insurance transaction; all that is required is that the provider of the insurance service undertakes to make a payment or provide a service on the materialization of a “risk”. By its decision, the FTT imported an additional feature, which is not one of the essential features of an insurance transaction as set out in the CJEU case law.

65. As regards the meaning of “risk” in this context, some of the language in the judgments of the CJEU might be taken to suggest that the insurance exemption is limited to cases involving an uncertain event that is adverse to the insured person. That is particularly so for those cases that refer to protections against “financial loss”. If that were the case, the exemption might be restricted to “indemnity insurance”, which provides compensation for a given loss of the insured person, and not extend to “contingency insurance”, which provides for a payment on a contingent event. If that were the case, the insurance exemption would not extend to the provision of many forms of life insurance (and not just those that are investment-based as the FTT suggests at FTT [137]).

66. Mr Bedenham submits that that conclusion cannot be correct; the insurance exemption must extend to life insurance contracts including those that perform an investment function such as that in Fuji. On his submission, the reference to a “risk” in the CJEU’s classic formulation of the essential features of an insurance transaction must be taken to mean simply a contingent “trigger event” for the payment or service in question. That event must be uncertain in that either the occurrence of the event itself must be uncertain or the timing of the event must be uncertain, but that is sufficient to meet the requirement for “risk”. Mr Bedenham relies upon the domestic case law in support of this submission and, in particular, Fuji.

67. As we have described above, following the decision in Gould, the domestic case law meaning of “insurance” under the Prudential test can extend to agreements under which an insurer makes a payment or provides a service on the occurrence of an uncertain event that is not necessarily adverse to the insured (and so can extend to life insurance contracts, including those with an investment element, such as that in Fuji). The CJEU case law relating to the insurance exemption from VAT does not address that issue. There is no CJEU decision on the application of the insurance exemption to life insurance contracts. If we had to decide the point, it seems to us that the rationale for the insurance exemption as described in the opinions of the Advocates General in CPP and United Biscuits (CPP AG [26] and United Biscuits AG [66] and footnote 54) and in the decision of the CJEU in United Biscuits (United Biscuits [32]) is capable of applying to at least some forms life insurance contract and possibly some forms of life insurance that involve an investment element. However, for the reasons that we give below, it is not necessary for us to reach a conclusion on that issue for the purpose of our decision on this appeal, and we do not do so.

68. Even if we accept that the concept of “risk” may extend to uncertain contingent events which may not be strictly adverse to the insured person, the more important question for the purpose of this appeal is whether it is implicit in the essential features of an insurance transaction as set out by the CJEU that a person other than the insured person bears the cost of the materialization of the relevant risk or uncertainty.

69. The FTT decided that it was. The FTT (at FTT [137]) refers to the need for the insurer “to assume a financial risk” for a transaction to be an insurance transaction for the purpose of the insurance exemption. At best, we suspect that the FTT’s statement slightly overstates the position. Even if it is an implicit requirement of an insurance transaction that a person other than the insured person bears the relevant risk or uncertainty, it is clear from the CJEU case law that it is not a requirement that the insurance service provider (i.e. the party to the contract with the insured person) ultimately bears the risk that is being covered. The risk may be borne by another person (see, for example, CPP [18] and Aspiro AG [22]).

70. In any event, Mr Bedenham submits that there is no such requirement and that by introducing this criterion the FTT erred in law by impermissibly adding to the essential features of an insurance transaction as prescribed by the CJEU. By reference to the domestic case law and the CJEU decision in Angel Lorenzo Gonzalez Alonso v Nationale Nederlanden Vida Cia De Seguros y Reasegouros SAE (Case C-166/11), he argues that it is not a necessary feature of an “insurance transaction” that the insurer (or a person other than the insured person) bears a financial risk.

71. We disagree with Mr Bedenham on this issue. Even if we accept for present purposes that the concept of “risk” may extend to an uncertain contingent event, in our view, it is a necessary implication of the essential features of an “insurance transaction” as expressed by the CJEU that, under the contractual relationship between the insured person and the insurance service provider, the insured person obtains some protection from the relevant risk or uncertainty. Under the arrangements as whole, the provider of the insurance service to the insured person may pass on the cost of providing that protection to another person (see CPP [18] and Aspiro [22]). But someone other than the insured person must bear the cost of the payment or the provision of the service that is provided on the materialization of that risk or uncertainty. Our reasons are set out below.

(1) As we have discussed, although the precise language that is used in the CJEU’s decisions may vary, the CJEU consistently refers to the insured person being protected in some way from “risk” (see [62] above). This is the essence of an insurance transaction within the insurance exemption (Mapfre [42]). That requirement cannot be satisfied where, as in this case, the cost of the payment or the provision of the service - on IML’s case, the provision of the death and life benefits - falls on the insured person - in this case, the member of the IM SIPP, through the member’s fund.

(2) Furthermore, as we have seen, the rationale for the insurance exemption is identified in United Biscuits (United Biscuits [32]) as being “the difficulty in determining the correct amount of VAT for insurance premiums relating to the coverage of risk”. No such difficulty arises if the insured person bears the relevant risk as no part of what he or she pays is a premium for the assumption of risk. We will elaborate on this point below, but, in this case, the member of the IM SIPP does not make any payment that can be regarded as a risk premium.

72. We acknowledge that the effect of our conclusion is that - even if the insurance exemption can extend to some life insurance contracts with an investment element - a distinction has to be made between cases (such as Fuji) where the premiums become owned by the insurance company and the cost of the payment benefits is made out of the insurance company’s own resources (even if the amount payable is notionally determined by reference to the value of underlying investments) and a case in which the premiums remain substantially owned by the insured person and the benefits are paid out of funds held substantially for the benefit of the insured person and/or other beneficiaries.

73. The pension arrangements, in this case, where the cost of the life and death benefits provided to the member is borne by a member’s own fund, fall within the latter category and outside the scope of the insurance exemption. We note that, in Winterthur, on similar facts to the present case, the tribunal came to the alternative conclusion largely because it took the view that the necessary obligation to make provide the life and death benefits could be found in the trust arrangements. Winterthur was, of course, decided some time before even the earliest of the CJEU cases to which we have referred (CPP) and accordingly the tribunal did not refer to the essential features of an insurance transaction as established in those cases. In our view, Winterthur is wrongly decided. If Winterthur was before us today, we would reach a different conclusion.

74. It follows that, although our reasoning may differ on some aspects, in broad terms, we agree with the FTT’s conclusions at FTT [141].

75. That conclusion is sufficient to dismiss this appeal. However, we will comment briefly on two related issues on which we heard argument from the parties.

Premium

76. The first is whether any payment made by the members of the IM SIPP can be regarded as a “premium”.

77. The essential features of an insurance transaction as specified by the CJEU require the “prior payment of a premium”. The CJEU case law does not focus materially on the meaning of a “premium” but rather on the assumption of risk (to which we have referred above). However, various points can be made from the case law:

(1) First, the premium must be paid in advance of the provision of the relevant benefit or service.

(2) Second, it follows from the rationale for the insurance exemption - being the difficulty in determining the correct amount of VAT for insurance premiums relating to the coverage of risk (United Biscuits [32]) - that a premium must involve some element of consideration for the assumption of risk by the other party (Mapfre [42], Aspiro AG [26]).

(3) It also follows that where it is possible to identify clearly a service to which consideration relates and that does not involve any element of risk, the payment is not a premium. This was the case in relation to the payments for the fund management services in United Biscuits (United Biscuits [31]) and the payments made for the sale of the motor vehicle parts in Generali (Generali [36]).

78. In the present case, Mr Bedenham says that the annual fees paid under the scheme rules and, to an extent, the contributions made by members constitute “premiums” for this purpose paid for the provision of the life and death benefits under the scheme. Mr Macnab says that none of the payments represents a premium. The contributions to the IM SIPP made by members are not consideration for any supply. The other payments and charges are paid for the list of services set out in clause 18 of the terms and conditions. They are not paid in advance. Annual fees are paid for the operation of the scheme as set out in the fee schedule; they are not paid for the provision of the life and death benefits under the scheme.

79. On this issue we agree with Mr Macnab.

80. The majority of the fees in the fee schedule are not paid “in advance” for a benefit that may or may not arise. They are paid either by the hour or as a fixed fee following the event in question. There are certain fees in the schedule that are paid in advance - in particular, the annual fees for the establishment and operation of the plan and the annual fees relating to property management and letting - but these are fees for specific ongoing administrative services provided to the member. They do not relate to the risk or contingency being, on Mr Bedenham’s case, the payment of the life or death benefits, and so cannot be regarded as “premiums”. The difficulty of charging VAT in relation to these amounts as described in United Biscuits [32] does not arise.

81. As regards the contributions made by the members to the fund, Mr Bedenham says that, at least in part, these contributions are made in return for the provision of benefits. In our view, the contributions to the fund cannot be consideration for any supply made by IML. All of the supplies made by IML under the arrangements are made in consideration for the various fees set out in the fee schedule. The contributions are made by the members to IML on the terms of the trust scheme and held by IML on the terms of the trust and the scheme rules. IML is not beneficially entitled to the contributions. They are invested under the terms of the scheme rules for the benefit of the member, his or her dependants and/or other beneficiaries.

82. Mr Bedenham points to the fact that there is provision in the terms and conditions of the IM SIPP which enables IML, as trustee, to sell investments to pay charges and fees. However, to our minds, it does not follow from the inclusion of that provision in the terms and conditions that the contributions are being made in return for the contingent payment of the life and death benefits or that the fees which are discharged from the funds are being applied in return for the contingent payments of the life and death benefits. The provision simply enables amounts that are beneficially owned by a member to be used to pay the charges and fees that are consideration for other services for VAT purposes.

Provision of a service under the contract

83. The second issue relates to the nature of the service provided under the contract.

84. As we have mentioned, on IML’s case, the service that it provided at the conclusion of the contract is the provision of the life and death benefits under the IM SIPP. Mr Macnab says that the life and death benefits cannot be the provision of the relevant service. The life and death benefits are provided to the members, their dependants, or other beneficiaries out of the members’ own funds in which IML has no beneficial interest. It is wrong to equate the duties and powers of IML under the trust deed and the scheme rules as a contractual obligation to provide benefits.

85. We also agree with Mr Macnab on this point. It seems to us that the only benefit or service that is being provided to the members (their dependants or other beneficiaries) when the life and death benefits are paid is the administrative service of releasing the funds. There is a separate charge for that service.

86. We note that in Winterthur, the tribunal found that the provision of pension benefits under the scheme in that case could amount to the provision of benefits under an insurance contract. The tribunal took the view that the trust arrangements could not dictate the VAT treatment and that the arrangements as a whole could be treated as comprising the necessary obligation. As we have mentioned above, Winterthur was decided before the any of the leading CJEU decisions to which we have referred. We would decide Winterthur differently today.

Conclusion

87. For the reasons that we have given, in our view, the supplies made by IML in connection with the provision of the IM SIPP do not fall within the insurance exemption. Our reasoning differs from that of the FTT on some of the issues, but our conclusion is the same. Any errors of law that the FTT may have made in reaching its decision were not material to the outcome and, on that basis, we will not remake the decision.

Disposition

88. We dismiss this appeal.

MR JUSTICE RAJAH

JUDGE ASHLEY GREENBANK

UPPER TRIBUNAL JUDGES

Release date: 26 September 2023

Annex

Annex to the FTT Decision: Terms and Conditions of the IM SIPP